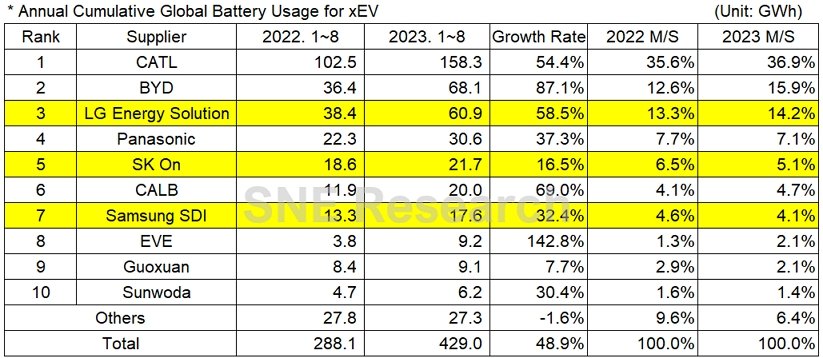

On August 3rd, the global information institution SNE Research released the global power battery installation data for the period from January to June 2023. Global battery enterprises submitted their performance for the first half of the year.

Overall, from January to June 2023, the global power battery installation volume reached 304.3 GWh, showing a year-on-year increase of 50.1%. This growth rate is slightly lower than the high growth rate of 71.8% for the full year of 2022. According to SNE Research’s initial estimate for the year, global power battery installations were projected to reach 749 GWh. However, achieving only half of this target in the first half of the year implies the need for considerable effort in the latter half.

Among these figures, the leading global power battery company, CATL (Contemporary Amperex Technology Co. Limited), achieved an installation volume of 112 GWh, representing a 56.2% increase compared to the same period last year. Its global market share stands at 36.8%, marking a 1.4 percentage point increase compared to the previous year. CATL remains the only power battery supplier with a market share exceeding 30.0%, consistently maintaining its global lead for six years.

Moreover, CATL’s battery installation volume is approximately equal to the combined volumes of the second, third, and fourth-ranking companies—BYD (47.7 GWh), LG Energy Solution (44.1 GWh), and Panasonic (22.8 GWh).

Regarding CATL’s sustained lead, SNE Research commented that based on the performance in the first half of this year, CATL has begun to surpass the domestic Chinese market and is rapidly expanding in overseas markets. The company’s battery installations in Europe and North America nearly doubled year-on-year. CATL’s batteries are primarily used in various vehicle models, including Tesla Model 3/Y, SAIC MG ZS, SAIC MG 4, GAC Aion Y, and NIO ET5.

Recently, CATL’s mid-year report for 2023 revealed the deepening global collaborations with Tesla, BMW, Daimler, Stellantis, VW, Volvo, Ford, Hyundai, Honda, and other automotive companies. The company’s overseas power battery usage market share from January to May this year reached 27.3%, a significant increase of 6.9 percentage points compared to the same period last year.

Benefiting from continued expansion in overseas operations and previous customer deliveries, CATL’s overseas sales revenue saw corresponding growth in the first half of this year. The company’s battery system products generated overseas revenue of 67.27 billion RMB, accounting for 35.49% of the total operating income, with a remarkable year-on-year surge of 195.15%. Notably, not only did this growth rate exceed the domestic revenue growth rate fourfold, but the overseas battery business also boasted a gross profit margin of 20.97%, higher than the domestic margin of 20.22%.

However, it’s worth noting that CATL’s battery installation growth rate of 56.2% in the first half of this year is almost half of the 111% growth rate achieved last year.

BYD, ranking second with 47.7 GWh, saw a staggering increase of 102.4% in installation volume year-on-year, leading to a rise in market share by 4.1 percentage points to 15.7%. The gap between BYD and the leader, CATL, decreased from 23.8 percentage points last year to 21.1 percentage points this year.

Interestingly, the ratio between CATL and BYD’s market shares (36.8% vs. 15.7%) in the first half of the year is proportional to their net profits. CATL achieved a net profit attributable to shareholders of 20.717 billion RMB, while BYD is expected to achieve a net profit of 10.5 billion to 11.7 billion RMB in the first half of this year.

SNE Research commented that BYD gains an advantage through its vertically integrated model of self-supplied batteries and automobile manufacturing. BYD’s electric vehicle models possess competitive prices, garnering significant popularity in the domestic Chinese market. Beyond China, particularly in Asia and Europe, BYD is expanding its market share, primarily focusing on models like the Atto 3 (Yuan Plus).

Moreover, based on BYD’s successful deployment of blade batteries for Tesla’s Model Y production in Berlin in the first half of 2023, BYD is positioned as a strong challenger to CATL in the future.

Looking at the overall performance of Chinese battery companies, apart from CATL and BYD, four other companies entered the top ten: Contemporary Amperex Technology Co. Limited, EVE Energy, Guoxuan High-Tech, and SVOLT Energy. The combined market share of these six Chinese enterprises reached 62.6%, significantly up by 5.9 percentage points from last year’s 56.7%.

Compared to last year’s top ten, EVE Energy replaced Farasis Energy. Notably, EVE Energy’s battery installation volume saw an astonishing year-on-year growth rate of 151.7%, ranking first among the top ten global power battery enterprises, along with BYD, achieving a triple-digit growth rate.

However, except for EVE Energy, the growth rates of the remaining three Chinese companies have considerably slowed compared to last year. For instance, SVOLT Energy’s battery installation growth rate dropped from 651% last year to 44.9% this year, EVE Energy from 163% to 58.8%, and Guoxuan High-Tech from 144% to 17.8%.

SNE Research noted that Chinese battery companies are currently advancing collaborations with South Korean companies. If South Korea, through a Free Trade Agreement (FTA) with the United States, provides battery materials for electric cars and exports them to American companies, it could meet the requirements of the “Inflation Reduction Act.”

In comparison, from January to June 2023, the market share of LG Energy Solution, Samsung SDI, and SK On from South Korea was 23.9%, a decrease of 2.2 percentage points from the same period last year. However, all three companies exhibited growth in battery installation volumes. LG Energy Solution’s 44.1 GWh saw a 50.3% increase year-on-year, ranking third. SK On installed 15.9 GWh, up by 16.1%, and Samsung SDI installed 12.6 GWh, up by 28.2%, ranking fifth and seventh, respectively.

The growth momentum of these three Korean companies is primarily due to the favorable sales of vehicles equipped with their batteries. Samsung SDI benefited from continued sales growth of BMW i4/7/X and Audi E-Tron. SK On showed growth momentum with strong sales of Hyundai Ionic 5, Kia EV6, and Mercedes-Benz EQA/B. LG Energy Solution gained sales boosts from globally popular models like Tesla Model 3/Y, Volkswagen ID.3/4, and Ford Mustang Mach-E, achieving the highest growth rate among the three Korean companies.

It’s worth noting that although LG Energy Solution was overtaken by BYD in market share, its battery installation growth rate increased significantly by 46.3 percentage points compared to the same period last year, despite a 4% market share decrease. This indicates a notable momentum. Additionally, the overseas sales of vehicles featuring LG Energy Solution’s batteries, such as Hyundai IONIQ 6 and Kona (SX2), are expected to expand, potentially benefitting future sales of LG Energy Solution’s batteries.

Panasonic is the only Japanese battery company to enter the top 10, with an installation volume of 22.8 GWh, representing a 39.2% increase from the same period last year. Its growth rate increased by 23.2 percentage points year-on-year, reducing its market share from 8.1% to 7.5%. Panasonic is one of Tesla’s main battery suppliers, accounting for the majority of Tesla’s models in North America. The sharp increase in sales of Tesla Model Y in comparison to the same period last year has contributed to Panasonic’s growth in battery installations.

Previously, the industry believed that Panasonic was showing signs of growth fatigue, but the current trends suggest otherwise, warranting further observation of the company’s market share changes.”

This translation might vary slightly in expression and structure to maintain readability in English while capturing the essence of the original text.

SNE research : https://www.sneresearch.com/en/insight/release_view/171/page/0

The most popular CATL cells : CATL 280Ah – Solargytech